Canonical Correlation Analysis¶

Canonical Correlation Analysis (CCA) is a statistical analysis technique to identify correlations between two sets of variables. Given two vector variables X and Y, it finds two projections, one for each, to transform them to a common space with maximum correlations.

The package defines a CCA type to represent a CCA model, and provides a set of methods to access the properties.

Properties¶

Let M be an instance of CCA, dx be the dimension of X, dy the dimension of Y, and p the output dimension (i.e the dimensio of the common space).

-

xindim(M)¶ Get the dimension of

X, the first set of variables.

-

yindim(M)¶ Get the dimension of

Y, the second set of variables.

-

outdim(M)¶ Get the output dimension, i.e that of the common space.

-

xmean(M)¶ Get the mean vector of

X(of lengthdx).

-

ymean(M)¶ Get the mean vector of

Y(of lengthdy).

-

xprojection(M)¶ Get the projection matrix for

X(of size(dx, p)).

-

yprojection(M)¶ Get the projection matrix for

Y(of size(dy, p)).

-

correlations(M)¶ The correlations of the projected componnents (a vector of length

p).

Transformation¶

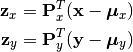

Given a CCA model, one can transform observations into both spaces into a common space, as

Here,  and

and  are projection matrices for

are projection matrices for X and Y;  and

and  are mean vectors.

are mean vectors.

This package provides methods to do so:

-

xtransform(M, x)¶ Transform observations in the X-space to the common space.

Here,

xcan be either a vector of lengthdxor a matrix where each column is an observation.

-

ytransform(M, y)¶ Transform observations in the Y-space to the common space.

Here,

ycan be either a vector of lengthdyor a matrix where each column is an observation.

Data Analysis¶

One can use the fit method to perform CCA over given datasets.

-

fit(CCA, X, Y; ...)¶ Perform CCA over the data given in matrices

XandY. Each column ofXandYis an observation.XandYshould have the same number of columns (denoted bynbelow).This method returns an instance of

CCA.Keyword arguments:

name description default method The choice of methods:

:cov: based on covariance matrices:svd: based on SVD of the input data

:svdoutdim The output dimension, i.e dimension of the common space min(dx, dy, n)mean The mean vector, which can be either of:

0: the input data has already been centralizednothing: this function will compute the mean- a pre-computed mean vector

nothingNotes: This function calls

ccacovorccasvdinternally, depending on the choice of method.

Core Algorithms¶

Two algorithms are implemented in this package: ccacov and ccasvd.

-

ccacov(Cxx, Cyy, Cxy, xmean, ymean, p)¶ Compute CCA based on analysis of the given covariance matrices, using generalized eigenvalue decomposition.

Parameters: - Cxx – The covariance matrix of

X. - Cyy – The covariance matrix of

Y. - Cxy – The covariance matrix between

XandY. - xmean – The mean vector of the original samples of

X, which can be a vector of lengthdx, or an empty vectorFloat64[]indicating a zero mean. - ymean – The mean vector of the original samples of

Y, which can be a vector of lengthdy, or an empty vectorFloat64[]indicating a zero mean. - p – The output dimension, i.e the dimension of the common space.

Returns: The resultant CCA model.

- Cxx – The covariance matrix of

-

ccasvd(Zx, Zy, xmean, ymean, p)¶ Compute CCA based on singular value decomposition of centralized sample matrices

ZxandZy.Parameters: - Zx – The centralized sample matrix for

X. - Zy – The centralized sample matrix for

Y. - xmean – The mean vector of the original samples of

X, which can be a vector of lengthdx, or an empty vectorFloat64[]indicating a zero mean. - ymean – The mean vector of the original samples of

Y, which can be a vector of lengthdy, or an empty vectorFloat64[]indicating a zero mean. - p – The output dimension, i.e the dimension of the common space.

Returns: The resultant CCA model.

- Zx – The centralized sample matrix for